The Greek ‘No’ referendum vote has an element of the Hong Kong Legislative Council’s resounding defeat of the political reform bill about it – telling an unelected, arrogant, dictatorial, soulless, distant supra-regime to drop dead. Since the country is going to default anyway, and the people will be penniless whichever currency it uses, we can only assume that the vote was primarily a gesture of defiance.

Another parallel is that in both cases the self-serving, grandiose autocracy (the Chinese Communist Party and the European Union) will probably carry on as if nothing had happened. The CCP was founded to liberate downtrodden workers from poverty, while the EU aimed to replace a perpetually warring continent with a peaceful free-trade zone. Both succeeded, and can go away now – but of course they are just getting started in their missions to be big, overwhelming, almighty and generally presumptuous towards the gods.

Even if the Brussels bureaucratic machine is oblivious to it, Greece shows the rest of us that the EU and its neo-imperial single-currency project is broken. Perhaps similarly,  China’s own debt problems are revealing the limits of CCP omnipotence. Specifically, the Great Patriotic Unburstable Stock Market Bubble Miracle looks like being Xi Jinping’s first visible and unmistakable screw-up.

China’s own debt problems are revealing the limits of CCP omnipotence. Specifically, the Great Patriotic Unburstable Stock Market Bubble Miracle looks like being Xi Jinping’s first visible and unmistakable screw-up.

The scales of the two failures seem to be quite different, so far.

The Euro was rooted in deranged megalomania. Euro-visionary elites salivated at the idea that their odd assortment of small-to-medium nation-states could be merged into a new, social-democratic version of the USA, so they could strut around on the world stage like American leaders, except sophisticated and pacifist. Since the populations of France, Germany, Italy, the Netherlands, etc irritatingly insisted on remaining sovereign, the utopians had to try constructing the new country backwards, starting with a flag (the easy bit) and then forcing them all to adopt the same currency and thus monetary policy. They are now locked in and uncompetitive with a voraciously mercantilist Germany, too ashamed to admit that it was a crazy idea.

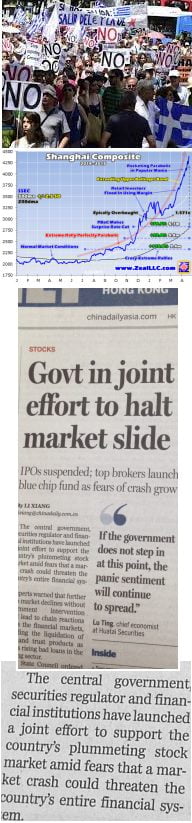

China’s debt problem looks relatively minor in historical terms. Insecure and fearful of popular unrest, the CCP ordered a mega-stimulus in 2008-09 and beyond. Billions directed into infrastructure investment ended up going into land and property speculation and bubbles. That felt good for a while and then became dangerous. But efforts to curb the bubbles threatened an economic slowdown, so the (still insecure and fearful) government talked up the stock market late last year apparently to divert everyone’s attention and spread joy and happiness throughout the land. The index more or less doubled in six months, and by the time millions of housewives and cab-drivers were piling into margin-trading accounts last month or so, the smart money started to come out – and no prizes for guessing what happens next.

Except the Chinese government is using every desperate measure to prop the market up, from freezing new issues to forcing brokerages and government funds to buy, buy, buy. Every time they succeed in reversing the declines in share prices and the index spikes 5%, rueful, not-so-smart money makes a dash for the exit. Unless it buys up the whole market, the Chinese government cannot halt this fall in stock prices from absurd ramped-up levels. But the concept of not being able to control is alien to the Communist mind.

Both the Euro as ‘a political not an economic project’ and China’s central-planning micromanagement of bubbles reveal stupidity at top policymaking levels. That stupidity has a human cost somewhere down there among the masses and lower orders. In Greece, elderly people wonder how they will pay for food, assuming they can find any in the markets. The Shanghainese mother-in-law of someone I know lost RMB500,000 on stocks. Good luck in restoring such people’s faith in their leaders.

Maybe both Europe and China will just ride out these crises – a Greek default and a Chinese stock crash don’t have to be the end of the world. But maybe this is just the beginning, and these man-made mistakes are going to trigger bigger and bigger disasters, from which none of us are spared. All we know for sure is that we are all being run by idiots.

It’s all very easy to blame the EU and/ or Germany. Why don’t you address the irresponsible PASOK policies that go back decennia and are the root of the Greek problem ?

Comparing the EU to the CCP is just silly.

A chief Economist at a HK bank explained much the same, that the Government was happy to see a rising stock market as it kept the populace happy. Blind Freddie could see that it would eventually end in tears.

On related affairs: just had lunch at that Chinese restaurant at Town Hall, Maxim I think. Will be closed at 1.30 as there is a DAB gathering tonight, several smelly flower arrangements already waiting. I wonder what they celebrate, Waiting for Uncle?

Good blog. Yes, besides feeling sorrow for the Greek people, I also got a kick out of seeing the unelected mandarins of the EU suffer a hiccup. Especially after the “it’s neck-and-neck!” polling reports all over the media before the vote. Let’s hope the whole failed project now stalls rather quickly, although I fear (as you mention) that they will just carry on regardless, or perhaps even find ways to (further) punish the Greeks for having the temerity to shape their own destiny.

Chinese policy-making sounds just like the children’s song about “The Old Lady Who Swallowed a Fly”.

The Greek referendum puts the spotlight on the EU’s democratic deficit, not that that has ever stopped them before.

If Greece is allowed to default n leave the currency the euro zone needs to make them leave the zone and shut the border. lest we will see the largest migration of greeks since the second world war as they use the last of their drachmas to buy some pretrol for the car n drive directly to the euro zone with nothing but a flash of their id card.

I hear that the African refugees who -unfortunately- landed in Greece are now paying operators to move them back to Somalia and such.

In Greece it is not unheard of that civil servants retire at the the ripe age of 45 with full pension and benefits which are then paid for by the tax payers of other EU countries.

Piketty: When I hear the Germans say that they maintain a very moral stance about debt and strongly believe that debts must be repaid, then I think: what a huge joke! Germany is the country that has never repaid its debts. It has no standing to lecture other nations.

https://medium.com/@gavinschalliol/thomas-piketty-germany-has-never-repaid-7b5e7add6fff

The Euro is a great idea in principle – after all, the world’s foreign exchange dealers are parasites who do nothing to create real wealth (i.e. produce useful goods and services), but merely shuffle stored wealth from one bit of paper to another, while taking a percentage of that wealth for doing so. However, a currency is only stable when its supply bears some relation to the amount of real wealth in the economy. For decades, unfortunately, governments and big banks have played fast and loose with the money supply, until the books could no longer be fiddled enough to hide the truth. The pity is that while these politicians and bankers retire to enjoy their accumulated hoard of Swiss francs, the ordinary people of Greece and other countries are expected to pick up the tab for their profligacy – an obligation they rightly resent.

http://www.theguardian.com/business/2015/jul/06/germany-1953-greece-2015-economic-marshall-plan-debt-relief

Greece’s finance minister at London Conference of 1953 signing a treaty agreeing to cancel 50% of Germany’s debt